What Does It Mean to Balance a Cash Drawer?

Balancing a cash drawer means verifying that the physical cash in the drawer matches what your records say should be there. At the end of a shift, a cashier counts every bill and coin, compares that total to the expected balance — what was in the drawer at open, plus sales collected in cash, minus any cash paid out — and records the result.

If those two numbers match, the drawer balances. If they don't, there's a variance. That variance could be an honest counting error, a transaction that wasn't logged, or something more serious. The goal of the balancing process isn't just to land on the right number — it's to create a reliable record that makes discrepancies visible and accountable.

How to Balance a Cash Drawer (Step by Step)

The process is straightforward, but consistency matters. Skipping steps — or doing them out of order — is where most errors creep in.

- Start with the opening float. Before the shift begins, count the starting cash and record it. This is your baseline. Without a documented opening count, you have no reliable way to reconcile what came in and went out.

- Track every transaction during the shift. Cash sales, cash refunds, and any cash paid out (petty cash, till pulls) should all be logged in your POS or register as they happen. A transaction that isn't recorded is a guaranteed discrepancy at close.

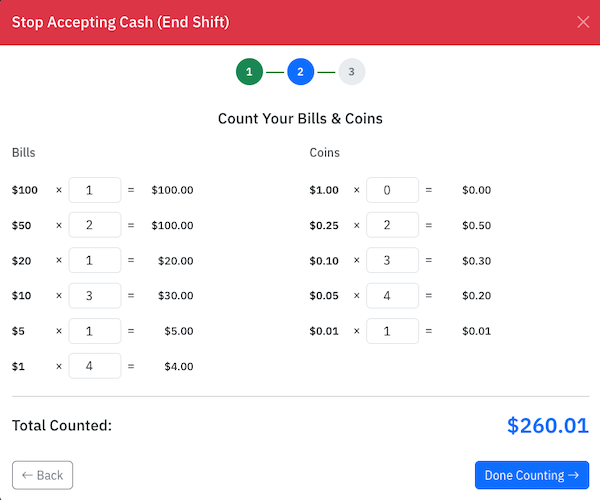

- Count the drawer at close — by denomination. Pull out all the cash and count it in groups: hundreds, fifties, twenties, tens, fives, ones, then coins. Write down each denomination count before adding them up. This slows you down just enough to catch mistakes.

- Calculate the expected balance. Opening float + cash sales − cash paid out = expected closing balance. Your POS should produce this number automatically.

- Compare counted cash to expected balance. If they match, the drawer balances. If not, you have a variance — record the amount and investigate before closing the session.

- Document and close. Record the counted total, any variance, and an explanation if there's a discrepancy. This becomes your audit trail for that shift.

Common Causes of Discrepancies

Most drawer imbalances trace back to a small set of recurring problems:

- Making change incorrectly. Giving a customer too much or too little change is one of the most common honest errors. High-transaction periods are where this happens most.

- Unrecorded cash-outs. Someone pulls cash for a small expense — a supply run, a tip-out — and forgets to log it. The money left the drawer legitimately, but there's no record of it.

- Missed voids or refunds. A transaction gets voided in the system but the cash was already returned to the customer — or vice versa.

- Counterfeit bills. A fake bill was accepted and counted as real. When it surfaces, the drawer comes up short against the actual value of legitimate cash on hand.

- Theft. Low-level skimming is more common than most owners expect, and it's often designed to stay just below the threshold where someone would investigate.

The challenge is that honest errors and deliberate ones look identical on a variance report. What separates them is the process you have in place before and after the count.

Best Practices to Prevent Errors

A good balancing process reduces errors before they happen, makes variance visible when it does, and creates the documentation needed to investigate and resolve it.

Count by Denomination, Not by Eyeballing

Counting a stack of bills as a lump sum is fast and almost always wrong. Count every denomination separately, write each total down, then add. This takes two or three extra minutes and catches transposition errors and miscounts that a fast flip-through misses entirely.

If you count twice independently and get two different numbers, count a third time. The right answer is in the drawer; your job is to find it.

Always Record the Opening Float

The opening count is the foundation of the reconciliation. If it's not documented, any discrepancy at close has two possible sources — something that happened during the shift, or an error in the starting balance — and you have no way to tell which. Record the opening float at the start of every session without exception.

Log Every Cash-Out

Unrecorded cash-outs are one of the most common sources of "mysterious" discrepancies. If cash leaves the drawer for any reason — a till pull, a petty cash expense, a refund — it should be logged in the system before it happens, not after. Build this into the habit rather than reconstructing it from receipts at close.

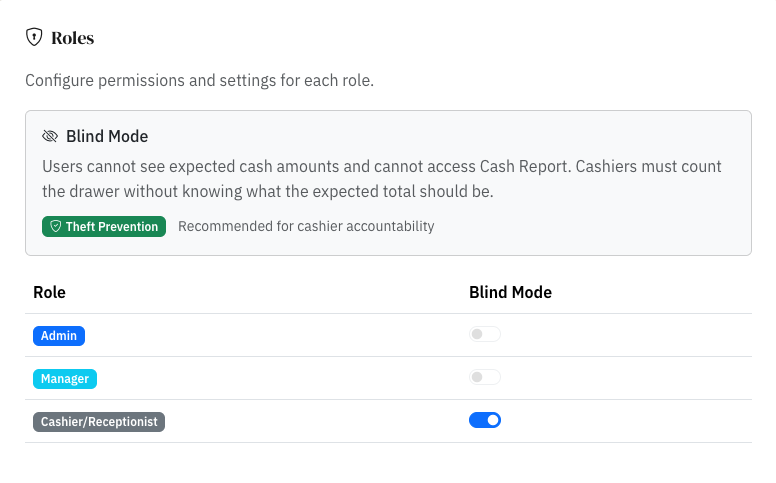

Use Blind Counting to Eliminate Bias

The subtler problem with cash counting isn't carelessness — it's that knowing the expected total before you count distorts the count itself. When a cashier sees "$342.50 expected," their brain works backward from that number. They count until they get close, assume a small miscount somewhere, and call it done. This is confirmation bias, and it's nearly universal.

The fix is blind counting: the cashier counts what's physically in the drawer and enters that number before the system shows any expected balance. The count has to be honest because there's no target to aim for.

RevenueRegister has a built-in Blind Mode setting that enforces this automatically for cashier roles. When enabled, cashiers count and submit their total without seeing the expected balance or the Cash Report. The system then compares their count to the expected balance, flags any variance, and requires a written explanation before the session can close. Managers and admins retain full visibility throughout — the control applies where it's needed without limiting the oversight your management team relies on.

Blind counting also deters theft. A cashier who can't see the expected balance doesn't know how much they can take and still "balance." That uncertainty is the deterrent — it removes the ability to game the system even before anyone tries.

What to Do When the Drawer Doesn't Balance

A variance isn't a crisis — it's information. Here's how to handle it:

- Recount before anything else. Most discrepancies under $5 are counting errors. Count again by denomination. If the number changes, you found it.

- Check for unrecorded transactions. Look for any cash that left or entered the drawer without being logged — a refund, a petty cash pull, a voided transaction. These are the second most common source of variances.

- Review recent transactions for entry mistakes. A sale entered as $54 when it was $45, or change made on a $20 when the customer handed over a $10, will show up here.

- Document the variance and your findings. Whether you resolve it or not, record what you found and why. A one-time $3 discrepancy that can't be explained is not a problem. The same cashier running $3–5 short every Friday is a pattern.

- Escalate patterns. A single unexplained variance warrants a note. Repeated variances on the same shift, with the same cashier, or trending in one direction warrant a conversation.

Common Mistakes That Cause Drawers to Come Up Short

Skipping the Opening Count

Without a documented opening count, you are just guessing. If the opening count is wrong, every downstream calculation is wrong. Make it non-negotiable: no transactions until the opening count is recorded and confirmed.

Counting Once and Trusting It

A single count is better than no count, but a recount is better still. This is especially true for large amounts or when something feels off. The few minutes it takes to verify saves the much longer conversation that happens when a session closes with an unexplained variance.

Letting Small Variances Slide

The instinct to wave off a $2 discrepancy is understandable but counterproductive. Small variances that go uninvestigated become the baseline expectation. They also mask patterns: a cashier skimming $2-3 per shift across dozens of shifts adds up, and it only looks like noise if no one is tracking it.

Not Explaining Discrepancies in Writing

Verbal explanations evaporate. A written note attached to the session — "customer was given wrong change on $60 transaction, reconciled with manager" — creates a record that's reviewable, searchable, and defensible. If the same explanation appears ten times across different sessions, that's a pattern worth investigating.

Showing Cashiers the Expected Balance Before They Count

This one is structural, not behavioral. When cashiers can see the expected total before counting, the count becomes a verification exercise rather than an actual observation. The solution isn't to ask them to ignore the number, it's to hide it until after they've submitted their count.

Frequently Asked Questions

How often should you balance a cash drawer?

At minimum, once per shift, at open and at close. High-volume operations often do a mid-shift count as well, especially if multiple cashiers share a drawer or if there are large cash transactions. The more frequently you count, the smaller the window for undetected discrepancies.

What's an acceptable cash drawer variance?

Most businesses tolerate variances of $1–2 per shift as rounding and change errors. Beyond that, consistent investigation is warranted. There's no universal threshold — what matters more than the amount is the pattern. A $10 variance once a quarter is very different from $5 short every Friday.

Should cashiers know the expected balance before counting?

No. Showing cashiers the expected balance before the count introduces confirmation bias — they will count toward the number rather than from the cash. This is true even for honest, diligent cashiers; it's a cognitive effect, not a character flaw. Use blind counting (or a tool like RevenueRegister's Blind Mode) to ensure the count reflects what's actually in the drawer.

What's the difference between a cash drawer and a till?

The terms are often used interchangeably. Technically, the "till" is the removable cash tray inside the drawer — the compartmentalized insert where bills and coins are sorted. The "cash drawer" refers to the full unit, including the till. For balancing purposes, the distinction doesn't matter much; you're counting everything in the till at open and close.

What should you do if you suspect theft?

Document everything before addressing it. Pull the variance records, note the pattern, and have your documentation in hand before any conversation happens. If your cash drawer system creates an audit trail — timestamps, session logs, variance history — that evidence is what turns a suspicion into a finding. Confront patterns, not individual events, and involve a manager or owner in any conversation that could have employment consequences.

RevenueRegister logs a full audit trail for every cash transaction automatically: who entered or modified the record, when the change was made, and any notes that were required to explain a variance. If a session is edited after the fact, the original entry and the change are both preserved with timestamps and the user's name attached. This makes it straightforward to reconstruct exactly what happened in a drawer session — and to show that reconstruction to anyone who needs to see it.

Ready to Put This Into Practice?

RevenueRegister gives your team structured cash controls from day one — opening counts, blind closing, variance tracking, and a full audit trail across every drawer and shift.

Start Your Free 14-Day Trial