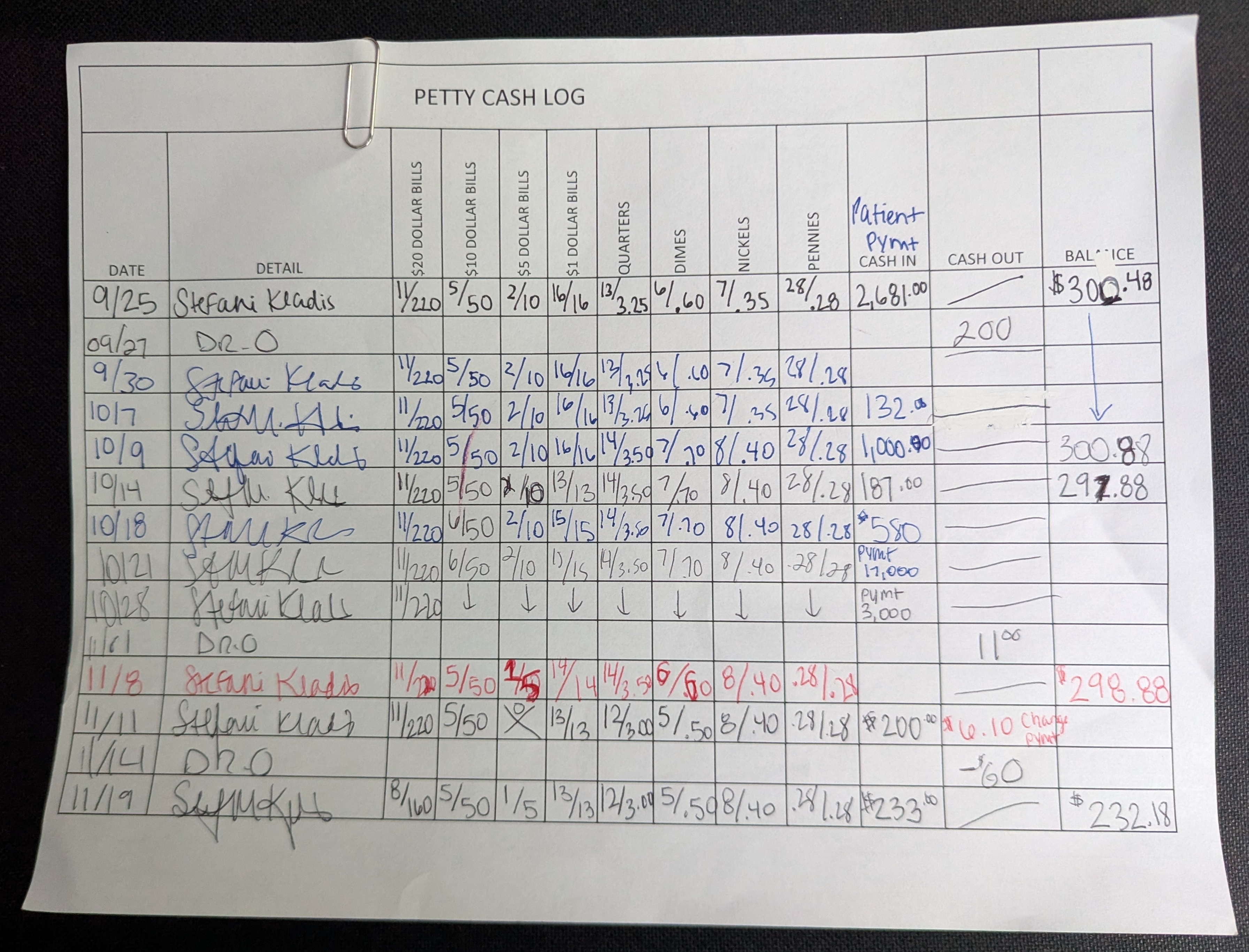

We come across a lot of cash logs in the field, but this one stopped us. A single sheet of paper, paper-clipped at the top, titled PETTY CASH LOG. Columns for every denomination — twenties down to pennies — a column for patient payments coming in, one for cash going out, and a running balance down the right edge. Handwritten, signed, corrected in three colors of ink. It's the kind of homegrown system that runs a real business, every day, right now.

And honestly? Whoever built it was thinking about the right things. There's real treasury instinct in this sheet. But there are also exactly the kinds of cracks that let money, and accountability, slip away quietly over months. Let's walk through it.

What This Log Gets Right

It's easy to dunk on a paper log. But before we do, credit where it's due: this sheet reflects better cash discipline than most small offices manage.

- It counts by denomination. The columns break the drawer down: 11 twenties ($220), 5 tens ($50), 2 fives ($10), and so on, all the way to "28 / .28" in pennies. Counting by denomination instead of just writing a single total is exactly how banks and retailers count a drawer. It forces the person to actually handle the cash, not estimate it.

- Every line is signed. Most rows carry a name in the detail column. Someone took responsibility for each count. That's the seed of an audit trail: the idea that every entry has an owner.

- It separates cash in, cash out, and balance. There are distinct columns for money coming in (patient payments), money going out, and the resulting balance. That's the correct mental model for a cash account, and a lot of informal systems never get even that far.

- It carries a running balance. The right-hand column tries to keep a live figure for what should be in the box — $300.48, then $300.88, $297.88, $298.88, down to $232.18. The intent is reconciliation: a number to count against.

In other words, the people behind this sheet understand that cash needs ownership, denomination-level counting, and a balance to check against.

Where It Starts to Break Down

Look a little closer and the cracks show. They're the expensive kind, because they're invisible until you go looking.

- Corrections everywhere, in different inks. The balance column is full of scratch-outs and rewrites. One figure reads "$300.48" with the 0 written over something else. An entry near the bottom is crossed out and rewritten in red as "$298.88." When the official record of your cash is also the thing you cross out and rewrite by hand, you've lost the one property an audit trail needs most: integrity. There's no way to tell a correction from a cover-up.

- The arrows that mean "same as last time." Several rows just have a downward arrow (↓) in the denomination columns, shorthand for "same as above." Look at the twenties: "11 / 220" repeats line after line, for weeks. Either this drawer genuinely never changed its twenties for a month, or, more likely, nobody actually recounted, and someone copied the previous row forward.

- Petty cash and patient revenue are tangled together. This is labeled a petty cash log, which is typically a small float for small expenses, balancing around $300. But the "Patient Pymt / Cash In" column shows entries of $2,681, $1,000, and even payments of $17,000 and $3,000. You cannot run $17,000 of patient revenue through a $300 petty cash box and have either record mean anything. Two completely different financial activities are being recorded in one place, and neither can be reconciled cleanly as a result.

- Cash out with no reason and no authorization. The "DR-O" rows (the doctor taking cash out) show $200, $11, and $60 leaving the box. No receipt reference, no stated purpose, no second signature approving it. Money simply leaves. In any controlled system, every dollar out needs a why and a who-approved-it. Here it's a name and a number.

- The balance doesn't cleanly walk. Try to follow the math: $300.48 → $300.88 → $297.88 → $298.88 → $232.18, against the cash-in and cash-out entries beside them. It doesn't tie out line to line. Somewhere in here the drawer is off, and the sheet has no way to tell you where, when, or by how much.

The Deeper Limitations

Even if every number on this sheet were perfect, the format itself imposes hard ceilings.

- One copy, one paper clip. This is the only record, and it's a loose sheet on a desk. A spilled coffee, a misfiled folder, or a busy front desk and months of history are gone. There's no backup, no version history, nothing.

- Dates, but no times — and gaps. Entries jump 9/25, 9/27, 9/30, 10/7, 10/9. What happened on the days in between? It could be that the practice wasn't open. Or it could be that the drawer was opened and transactions were made but weren't recorded.

- No blind count. The person writing the count can see the expected balance sitting right there in the previous row. That defeats the entire purpose of a count. A real control is a blind count: you record what you physically have before the system shows you what it expects. This sheet shows you the answer before you've done the work.

- No way to attribute an error to a moment. If the box is short $68 at month's end, this sheet can't tell you which day, which shift, or which person was responsible. Without that, a shortage is never anyone's fault, which means it's never resolved, and never deterred.

- It doesn't scale past one box. One drawer, one location, one sheet. Add a second register or a second office and you're back to paper-clipping more pages and hoping they reconcile.

How You'd Fix Each of These

The fixes aren't exotic. They're the same controls a bank teller line uses — just applied to a petty cash box. Map them one to one against the problems above:

- Make the record immutable. Entries should be logged, timestamped, and attributed. Corrections should be tracked as corrections, not erasures. You keep the full history, including what changed and who changed it. No more guessing whether a red-ink rewrite was a fix or a cover.

- Force a real count, every time. Replace the "same as above" arrow with an actual denomination entry each session, and hide the expected total until the count is submitted. This is called a blind count. Now the number on the page is something someone genuinely counted.

- Separate petty cash from revenue. Patient payments belong in revenue tracking; the petty cash float is its own small, bounded account. Keep them in distinct records and each one stays reconcilable. A $17,000 payment never lands in a $300 box again.

- Require a reason and an owner for every cash-out. Money leaving the drawer gets logged with a purpose and tied to the person who took it. So "DR-O, $200" becomes a documented, reviewable transaction.

- Attribute every session to a person and a time window. When the box is short, you can see exactly which session it happened in. Errors get isolated and resolved instead of written off.

- Back it up and let it scale. Records live in software, not on a desk. Backed up, searchable, and ready for a second drawer or a second location without a single new paper clip.

This Is Exactly Why We Built RevenueRegister

RevenueRegister takes every instinct that handwritten log got right — denomination counting, signed ownership, a running balance — and removes every weakness that paper forces on you.

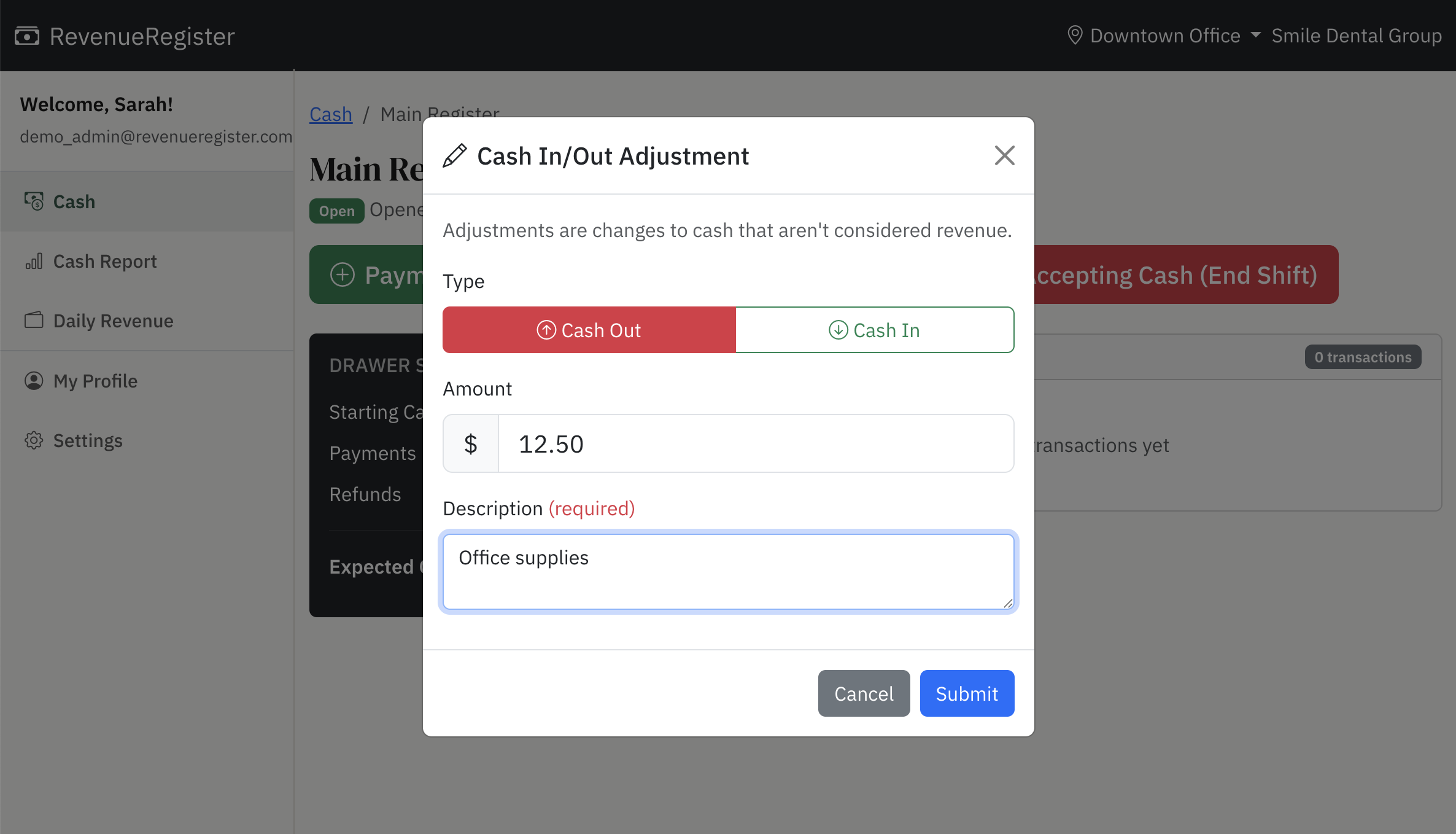

You open a drawer session tied to the person running it. You record cash in and cash out as it happens, each cash-out with a reason. For added security, you close with a blind count — you enter what you physically counted, by denomination, before the system reveals what it expected — and any discrepancy is surfaced immediately, attributed to that session, that person, that moment. Petty cash and daily revenue are tracked as the distinct things they are. Nothing is crossed out in red; corrections are tracked, not erased. And it all scales from one box to many drawers across many locations, with role-based access so staff record what they need and admins see everything.

The office behind that paper log was doing better than most. They cared, and it showed. They just didn't have a tool built for the job, so their good instincts leaked through the cracks in the medium. Strict cash controls shouldn't require perfect handwriting and a steady supply of paper clips.

If your business still runs on a sheet like this one, you don't need to abandon what you're doing well. You need a system that makes the right way the easy way, and makes fraud, theft, and honest mistakes far harder to hide.